Saving and investing money on behalf of children or grandchildren could make a big difference to their future, helping them to pay for university or even put down a deposit on their first home.

A simple and tax-efficient way to save money for children is to invest through a Junior ISA. If you begin early, your child or grandchild could have a substantial sum of money by the time they turn 18, giving them an important financial leg up as they enter adulthood.

Why invest for a child?

Children today face a more uncertain financial future than they did in the past. University tuition fees in the UK have increased nine-fold since 1998 to up to £9,250 a year[1], meaning many students face graduating with enormous levels of debt.

Meanwhile, house prices have increased at a much faster pace than average wages, making it harder to get a foot onto the property ladder.

Investing for your child or grandchild offers them the chance to graduate free from debt, raise a deposit for their first home, or simply have a financial boost when they most need it.

Cash versus investing

There are lots of options when it comes to saving and investing money for children. Piggy banks and cash savings accounts are useful for teaching young children about money, as well as funding short-term goals like buying a new gadget or toy. But when it comes to longer-term goals, leaving money in cash probably isn’t the wisest decision.

The interest rates on cash savings accounts tend to be below the rate of inflation. This means that, over time, the ‘real’ value of your child’s savings will decline. If you left £100 in a piggy bank and inflation averaged 2.5% a year, its real value would fall to just £53.10 after 25 years.

Investing in the stock market offers the potential for greater long-term growth, helping your money to work harder for your child’s future. Although the stock market is volatile, history shows that over periods of ten or more years it tends to perform more strongly than cash and grow above the rate of inflation.

The benefits of a Junior ISA

One of the best ways to invest for a child’s future is through a Junior ISA. You can invest up to £9,000 a year (tax year 2023/24) for each child, and you don’t pay capital gains tax on the profits (‘gains’) you make when selling investments.

Reinvested interest and dividends are also tax free, making Junior ISAs a simple way of investing tax efficiently. Once your child turns 18, they can either access the money or continue investing through an adult Investment ISA.

Although it’s possible to invest for children through your own ISA, opening a Junior ISA means you won’t use up any of your own £20,000 annual ISA allowance. You might also find it easier to manage your savings and investments if you can clearly see how much money belongs to each member of the family.

Other family members can also contribute to your child’s Junior ISA, helping to build up an even more substantial sum of money.

How much to invest

How much you choose to invest will depend on a range of factors, including your financial circumstances, goals, and personal preferences. It’s important to ensure you don’t invest more than you can afford, and that you’re not neglecting other goals, such as saving for your retirement.

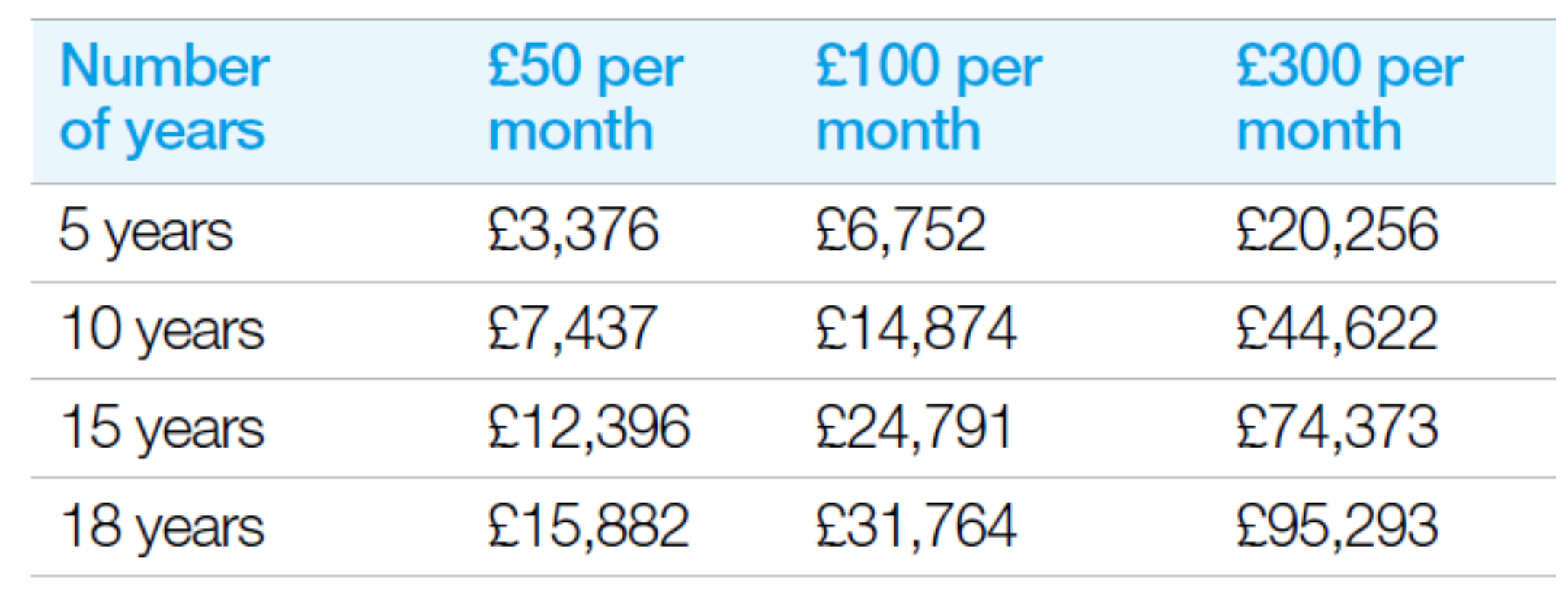

The table below gives an illustration of how much a monthly investment could potentially be worth after five, ten, 15 and 18 years. Remember, investments can fall as well as rise, and inflation can reduce the spending power of money over the long term.

Source: RBC Brewin Dolphin. Assumes investment growth of 4% a year after charges and before inflation.

The key thing to remember is that the earlier you start, the better your chances are of boosting your child’s future financial security. Not only will you be saving for a longer period, but you’ll also have longer to potentially benefit from investment growth and compound returns. Compounding is where you get a return on your returns as well as on your initial capital, and it is particularly powerful over long periods.

Next steps

Understanding how much you can afford to save for children and where to invest it isn’t always straightforward. Taking some smart advice will help you feel confident that you’re balancing saving for children with your other needs, and that you’re on track to meet all your goals. Because good decisions follow smart advice.

Disclaimer

The value of investments, and any income from them, can fall and you may get back less than you invested. This does not constitute tax or legal advice. Tax treatment depends on the individual circumstances of each client and may be subject to change in the future. Information is provided only as an example and is not a recommendation to pursue a particular strategy. Information contained in this document is believed to be reliable and accurate, but without further investigation cannot be warranted as to accuracy or completeness. Forecasts are not a reliable indicator of future performance.

RBC Brewin Dolphin is a trading name of Brewin Dolphin Limited. Brewin Dolphin Limited is authorised and regulated by the Financial Conduct Authority (Financial Services Register reference number 124444) and regulated in Jersey by the Financial Services Commission. Registered Office; 12 Smithfield Street, London, EC1A 9BD. Registered in England and Wales company number: 2135876. VAT number: GB 690 8994 69.

[1] www.ucas.com/finance/undergraduate-tuition-fees-and-student-loans and https://commonslibrary.parliament.uk/research-briefings/cbp-8151/